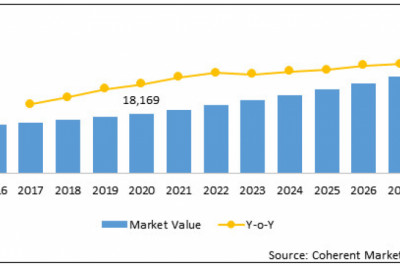

Welding Consumables Market size is forecast to reach $13.9 million by 2025, after growing at a CAGR of 5.9% during 2020-2025, owing to the increasing demand for welding equipment and consumables from various end-use industries such as automotive & transportation, aerospace & defense, building & construction, and more. The demand for welding consumables is increasing in varied industries as it is the most efficient method to obtain reliable, precise, cost-effective joints in manufacturing industries. Furthermore, the adoption of welding consumables has increased over the past few years, owing to the rapid growth of fabrication and manufacturing industries in various regions. All these factors are anticipated to drive the welding consumables market substantially during the forecast period.

Welding consumables Market Report Coverage

The report: “Welding Consumables Market – Forecast (2020-2025)”, by IndustryARC, covers an in-depth analysis of the following segments of the welding consumables Industry.

By Type: Stick Electrodes, Solid Wires, Flux Cored Wires, SAW Wires & Fluxes, and Others

By Technique: Arc Welding, Resistance Welding, Oxy-Fuel Welding, Laser-Beam Welding, and Others

By End-Use Industry: Automotive & Transportation, Aerospace & Defense, Building & Construction, Energy, Heavy Machinery, Marine, and Others

By Geography: North America, South America, Europe, Asia Pacific, RoW

Key Takeaways

Asia Pacific dominates the welding consumables market, owing to the increasing demand for welding from the automotive industries to manufacture parts of the automobiles. According to OICA, the production of light commercial vehicles has augmented by 10.2 % in 2018 in the APAC region.

Welding is a reliable, precise, high-tech, and cost-effective method for joining materials, such as metals and alloys, efficiently in various manufacturing industries. These consumables are flux & filler materials used in the welding industry and are generally used in arc welding processes.

A gasless mig welder is lighter and portable to carry. Also, there is no need to clean and shine the surface before welding when using a gasless mig welder as flux here enables to weld through rusted, painted, or galvanized surface with much ease. Thus considering these factors, its demand is increasing for industrial projects.

The welding consumables liquify while joining metals and assist in producing a firm joint. They also shield the molten weld from atmospheric contaminants. Stainless steel welding rod, aluminum welding rods, and copper welding rod are mostly utilized welding consumables.

Due to the COVID-19 Pandemic, most of the countries have gone under lockdown, due to which operations of various industries such as automotive and aerospace have been negatively affected, which is hampering the welding consumables market growth.

Welding consumables Market Segment Analysis - By Type

The flux-cored wire segment held the largest share in the welding consumables market in 2019, owing to its superior properties to other types of welding consumables. The flux-cored wire does not require external shielding gas because the weld pool is protected by gas generated when flux from the wire is burned. As a result, the flux-cored wire is more portable because it does not require an external gas tank. Also, they allow for a high deposition rate and work well outdoors and in windy conditions. With the right filler materials, these electrodes can make FCAW an all-position process, which is anticipated to boost the demand for flux-cored wire as a welding consumable during the forecast period.

Welding consumables Market Segment Analysis - By End-Use Industry

The automotive and transportation application held the largest share in the welding consumables market in 2019 and is growing at a CAGR of 7.5%, owing to the wide usage of welding consumables in the automotive industry for nearly every new vehicle design. In the automobile industry, welding consumables are used in the production of lightweight and high-quality vehicle parts. Improvements in the safety features of vehicles, along with evolving automobile designs, have escalated the sales of automobiles, thereby bolstering the growth of the welding consumables market. Arc welding is widely used for chassis parts in the automotive industry to ease the continuous joining and to secure high strength and rigidity of joints and wide freedom of joint shape to allow easy joining to pipes, brackets, or other accessories. The wide usage of welding in the automotive industry is expected to increase the demand for welding consumables from the automotive and transportation sectors during the forecast period.

Welding consumables Market Segment Analysis - By Geography

Asia Pacific region held the largest share in the welding consumables market in 2019 up to 38%, owing to the rise in demand and production of automobiles in the region, due to the increasing population. In 2018, according to OICA, the automotive production in India, Thailand, Indonesia, and Malaysia has increased up to 5174645, 2167694, 1343714 and 564800, i.e., 8.0%, 9.0%, 10.3%, and 12.2% higher than the previous year due to rising per capita income of the individuals which further led to the massive demand for advanced automotive machines manufacturing in the APAC region. According to the International Trade Administration (ITA), China is the world’s largest vehicle market and the Chinese government is expecting that automobile production will reach 35 million by 2025. In 2018, according to the China Association of Automobile Manufacturers, over 27 million vehicles were sold in the country. According to the International Organization of Motor Vehicle Manufacturers, the total production of the automobile (commercial as well as Personal) globally in the year 2019 was 91,786,861 units compare to 96,869,020 units in 2018. Whereas, the total production of the automobile (commercial as well as Personal) in Asia-Pacific in the year 2018 was 52,449,078 units compared to 53,395,211 units in 2017. The increase in global automobile production is a major factor leading to the growth of the Welding Consumables Market in the APAC region.

Welding consumables Market Drivers

Increasing Aerospace Industry

There is an increasing demand for welding consumables from the aerospace sector for joining parts such as gas tungsten arc, plasma arc, and gas metal arc in the aircraft. It is largely used to join metal matrix composites and ceramics as well as ceramics to metals, and also nickel-base and titanium-base alloys. According to the International Trade Administration (ITA), in 2019 China was the world’s second-largest civil aerospace and aviation services markets and one of the fastest-growing markets. In 2016, according to Boeing, China is estimated to require around 6,810 new commercial aircraft, valued at USD 1 trillion, over the next two decades. By the end of 2018, China had more than 59 airlines and 3,615 civil aircraft (an increase of 10% over 2017). According to China’s 13th Five Year Plan (2016-2020), by 2020, China will have more than 4,500 civil aircraft, and by 2018, the number of Chinese civil airports had grown to 235. According to the International Trade Administration (ITA), in 2018 the Indian government spent a total of $645 in the civil aviation sector. Also, according to Boeing India is expected to drive the demand for 2,300 aircrafts worth US$320 billion over the next 20 years. Thus, the increasing aviation industry acts as a driver for the welding consumables market.

Increasing Building and Construction Activities

There is an increasing demand for welding consumables form the building and construction activities. The building and construction activities often require a welding method to connect the steel I-beams, columns, trusses, and footers that make up the structural framework of a building. These components are cut to size, lifted into position with a crane or construction jack, and then welded together to support the floors, walls, and roof of a building. According to the US Census Bureau, in February 2020 total construction was at a seasonally adjusted annual rate of 1,366,697 which is 6.0 percent above the February 2019 rate of 1,288,951. According to the European Commission, the total construction investment in Germany increased by 9.5% over 2008-2015. Also, the European Construction 2020 Action Plan aimed at stimulating favorable investment conditions. The building and construction activities are also increasing owing to the various government initiatives such as Foreign Direct Investments (FDI). Thus, with the increasing building and construction activities in the region, the demand for welding consumables will also substantially increase, which acts as a driver for the welding consumables market during the forecast period.

Welding consumables Market Challenges

Expensive Metal Fabrication Operation and Shortage of Skilled Labor

Metal Fabrication is a primary operation in various end-use industries that uses sheet metal fabrication processes for product restoration, customization, and roll cage fabrication with high manufacturing cost. The major factor hampering the industry growth is the high cost of metal fabrication tools limiting the designing and crafting of highly complex geometric shapes, as compared to plastic fabrication machines. Moreover, metal fabrication requires post-fabrication processes, such as deburring, finishing, and panting, which is a time-consuming and costly operation. Furthermore, the unavailability of the skilled labor force is posing a challenge to metal fabrication industrial growth. The lack of investment in rigorous training and development of local laborers is leading to the shortage of a skilled workforce.

Covid-19 Impact on The Welding Consumables Market

Due to the pandemic, there’s been a supply chain disruption in the global and local enterprises which are dealing with the manufacturing of welding consumables. Due to the coronavirus, the production in these sectors is expecting to experience difficulties like untimely deliveries of welding consumables. In addition, the COVID-19 outbreak is having a huge impact on the automotive industry. The production of automobiles has been disruptively stopped, contributing to a major loss in the total automotive sectors. There has been a temporary suspension of automotive production in various regions. According to the European Automobile Manufacturers Association, In June 2020, demand for new commercial vehicles across the EU remained weak (-20.3%). With the decrease in automotive production, the demand for welding consumables has significantly fallen, which is having a major impact on the welding consumables market.

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the welding consumables market. In 2019, the market of welding consumables has been consolidated by the top five players accounting for xx% of the share. Major players in the welding consumables market are Ador Welding Ltd., Arcon Welding Equipment, LLC., AV Weldtech Pvt. Ltd., Anand Arc Ltd., D & H Welding Electrodes (India) Ltd., Denyo Co., Ltd., EWAC Alloys Ltd., GEE Limited, INOX Air Products Private Limited, Ketan Corporation, Praxair Incorporated, Precision Weldarc Limited, The Linde Group, Welmet Technologies Private Limited, and Yenitek Corporate Group.

Acquisitions/Technology Launches

In September 2019, Lincoln Electric Introduced new GTAW (TIG) cut lengths with high silicon formulations using stainless steel alloys for the clean and high-quality welding process. Upgraded manufacturing processes for the new products are enhancing the quality of the product by reducing complexities in the welding process.

In July 2019, ESAB launched new cut master black series with an enhanced feature by plasma cutting of consumables. This feature extends the operating life of the welded wires and electrodes by 60% that comes with a cut master 60ihandheld air plasma cutting system.

For more Chemicals and Materials related reports, please click here