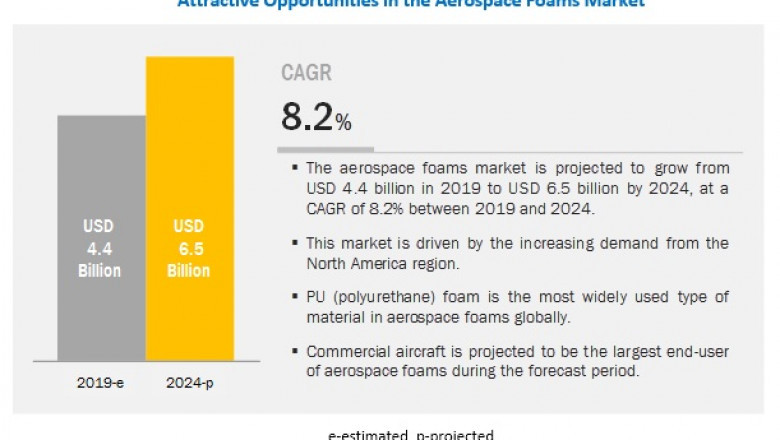

The aerospace foams market is projected to grow from USD 4.4 billion in 2019 to USD 6.5 billion by 2024, at a CAGR of 8.2% from 2019 to 2024. The rising demand for lightweight and fuel-efficient aircraft have led to the extensive use of advanced materials such as PU foams, PE foams, and others, in the aerospace industry. The manufacturing of advanced materials as well as new product launches by many prominent players in the aerospace industry is one of the key factors driving the growth of the aerospace foams market across the globe.

Based on end-use, the commercial aircraft segment led the aerospace foams market in 2018 in terms of both value and volume. The growth of this segment can be attributed to the increase in the number of air passengers and high demand for low-cost operators in the regions such as Asia Pacific, Middle East, and South America is driving the growth of the commercial aircraft segment. Furthermore, the surge in the growing demand for LCC from Southeast Asia, India, and Australia is aiding in the growth of the overall commercial aircraft segment and thus propelling the demand for aerospace foams as well

BASF SE (Germany), Evonik Industries AG (Germany), Boyd Corporation (US), Rogers Corporation (US), FoamPartner (Switzerland), Armacell International S.A. (Luxembourg), SABIC (Saudi Arabia), ERG Materials and Aerospace Corp (US), UFP Technologies, Inc. (US), Zotefoams Plc (UK), General Plastics Manufacturing Company (US), Solvay SA (Belgium), Pyrotek Inc. (US), and Greiner AG (Austria) are some of the leading players operating in the aerospace foams market.